Want To Grow Your Net Worth?

September 23, 2019

If you want to grow your net worth, you are going to have to do things right, which can be uncomfortable.

1. Make Sacrifices - a Temporary Set Back could Lead to a More Prosperous Future

Spending less now may help to achieve two things:

- Build an emergency pot of funds

- Build up surplus income / capital for anything else

The amount to save will vary depending on your preferred lifestyle, on a joint/single income and whether you already have access to readily available funds. As a rule of thumb, we advise on putting away six months’ worth of expenses. Saving as much of your income as possible is a good start, but it’ll only get you so far- therefore it’s a good idea to start planning early and consider investing your surplus funds.

Not every season is a harvest one, but resisting short term temptations will help to reap future gains.

2. Shake Up Your Finances

For those already with assets/wealth, you can consider shaking up your finances. Sometimes you can maximise your overall wealth by simply restructuring your assets, mainly driven by sensible taxation planning. For example,

- By simply structuring debt correctly (not all debt can be classified as bad)

- Converting income to capital gains (income tax tends to be higher than capital gains tax)

- Utilising tax relief

3. Hoist Your Sail to Capture those Winds (Returns)

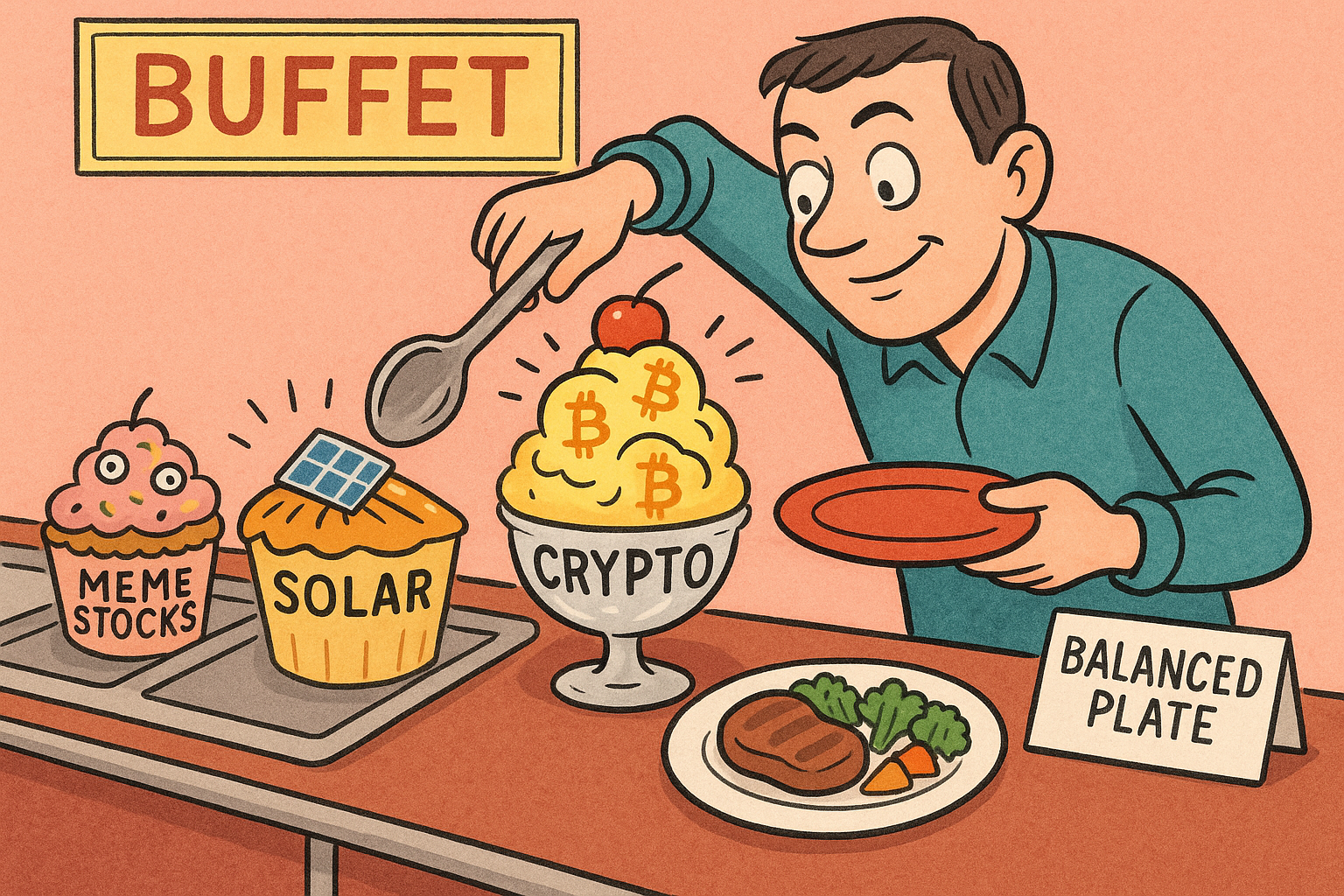

To truly maximise your income/capital’s potential, you’re going to have to do more than keeping it in a savings account.

For instance, a £100,000.00 savings in a current account may attract 0.5% return (we are being very generous here), will result in a guaranteed loss once we factor in inflation which is currently running at 1.7% (August 2019 CPI). However, for the very short term, savings accounts are okay. For a longer investment time horizon, it can be sensible to split your investments into retirement and non-retirement pots. An investment account that allows you to contribute and withdraw from will give you flexibility.

Investing comes with risk, but so is avoiding it, in the sense that your wealth may not keep up with inflation. There are plenty of empirical data that supports long-term patient investing, generates real positive returns with far more certainty than investing over a short period of time, say a year.

Next Steps

No matter where you are at your wealth building journey, it’s never too late to make a start. Taking baby steps is better than not trying at all. Start planning now, and by doing so you may be able to retire earlier, go on nicer holidays (who doesn’t want that?), have a better future planned for your family or buy that dream house / car.

Risk Warnings:

The information contained in this article is intended solely for information purposes only and does not constitute advice. The price of investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested. Past performance is not necessarily a guide to future performance.

The Iron Wealth Blog

When Markets Don’t Feel Fair: How We Reduce the Risk of Being on the Wrong Side of the Trade

In the world of investing, there is always something trending and receives a lot of attention.

We've been taught to save for a rainy day, which is wise to some extent. However, keeping all your money in cash over the medium to long term carries risks, too. In fact, doing nothing with your money is the biggest risk of all, as inflation will erode its value over time.

We are 5! This month we are celebrating Iron Wealth turning 5 years old. We are so ever thankful for everything we have achieved.

Is it worth switching your investment portfolio to cash? In this blog, we discuss why cash isn't all it's hyped up to be, even at 5%.

There is no better time to size your unsheltered portfolio correctly.

Fact: They are rare, inevitable and are a feature of the markets.

An Alternative Source of Income/Capital: Equity Release & Retirement Mortgage

A common question that you may have heard or asked is “What is the income/yield?” But have you truly thought about the meaning of this question? Firstly, what do they mean by “yield”? Yield is what you get back from your investment, the interest or dividend you receive. Many people like the thought of a stable, sustainable income and therefore, they focus on obtaining a high income. This is especially true for those approaching and/or in retirement. After Years of earning a regular income through our wages, we are bias towards continuing this approach with our pensions and investments. This is another reason why most people would opt for an income stream in the form of a final salary pension over a lump sum. We saw an example of this when Camelot launched ‘set for life’ in 2019, where instead of winning the jackpot as a lump sum, the winner would receive £10,000 a month for life. A lump sum has its benefits too, it gives us flexibility, control, inflation proofing and the ability to manage counterparty risk (the probability of default). Of course, this all depends on individual circumstances and objectives. If you structure an investment portfolio for maximum income/yield only, or as your main objective, you distort the portfolio, leading to far higher risks and can potentially lead to higher taxation in the future.

As the impact of COVID continues to adversely affect business, it looks like further redundancies are inevitable. This may sound grim, but you can lessen the blow by getting financially prepared. For those who are still in employment and are facing potential redundancy, sometimes it helps to take a step back to see the bigger picture. Here are some questions that you can ask yourself? 1. Are you ready to take early retirement? 2. If not, how quickly can you get another job and at what pay? 3. How big is the carrot? 4. Do you want to retire now or do you want to tie this in with your partner? 5. Are you in good health? 6. What do you have planned for retirement? i.e. if it is travelling the world, then probably not the right time 7. What’s the job security like for your partner?